Interest-bearing accounts

Banks and financial institutions offer various types of accounts that can earn interest, including savings accounts and deposit accounts. These accounts are typically used for short-term savings, emergency funds, specific goals like travel or major purchases, or as part of a diversified investment strategy. They provide a safer alternative to riskier investment options and offer a convenient solution for saving money while accruing interest. These accounts can often be created as sub-accounts by account holders through their banking apps.

The Pismo platform offers an API that supports a wide range of interest-bearing accounts, including savings and deposit accounts, all capable of performing daily interest calculations and payouts as well as on a monthly, quarterly, semi-annual, annual basis, or at its maturity.

Pismo offers the following bank account products, each with its own specific rules and benefits:

-

Savings account product: These accounts can be created as sub-accounts in banking apps, allowing for easy deposit and withdrawal of funds.

-

Deposit product: Also known as Certificates of Deposit (CDs), these accounts have a preset maturity date. Customers must leave their money in the account for an agreed-upon term. Early withdrawals may incur fees, and these accounts often have a minimum deposit requirement, a maximum balance limit, and a cooling-off period. They offer various rule possibilities, making them versatile for clients looking for different interest calculation options.

The return, interest rate, and other features of these accounts depend on the account terms and conditions and can vary based on the account type and the financial institution. They might require a minimum deposit or balance, have restrictions on withdrawals and transfers, and the terms can change over time.

Deposit accounts are particularly popular on the Pismo platform due to their ability to support multiple rule possibilities, while savings accounts remain more basic. The interest-bearing accounts solution from Pismo is notable for its robust capability to process large volumes of daily operations, fully customizable fee and interest calculations, and the generation of legal reports.

This guide provides information on the available options to set up interest-bearing accounts on the Pismo platform, including common parameters, outputs, and examples.

Interest-bearing accounts on the Pismo platform

Banking by Pismo

If you maintain accounts in the Pismo platform as part of its core banking solution, you have seamless access to the products and solutions offered by Pismo and are uniquely set up to take advantage of their flexible configurations and high-capacity processing.

In this case, work with the Pismo representative to set up interest-bearing accounts. Note that you can also set up the following steps in Pismo Control Center:

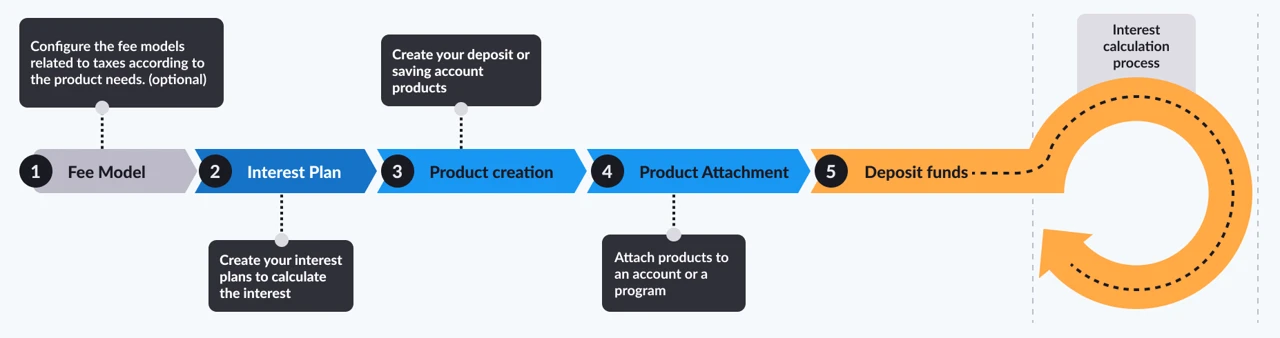

Figure 1: Pismo banking workflow

- If applicable, set up the fee model in the Pismo platform to withhold any taxes or operational fees. Refer to Fee models for how to set this up in Control Center.

- Configure a flexible plan to accrue interest according to your needs. To set this up in Control Center, refer to Interest plans.

- Create a product (Savings or Deposit product) in the Pismo platform. Refer to Deposit products if you want to configure it using Control Center.

- Attach the product you created to specific accounts or all accounts in a program. Note that you cannot attach more than one product to the same program or account.

- Once complete, events are generated to notify you of the interest to be posted. For more information, refer to Output events.

Minimum amount for interest calculation

- You have the option to specify a minimum amount used for interest calculation, either at the program level or for a specific account ID. specify a value in the

min_amountfield of Create deposit product or Create savings account product. If you choose not to set a minimum, interest is calculated on any amount.

Pismo integration with other banking systems

If you maintain accounts in a different core banking system outside of Pismo, you can still utilize the Pismo platform to offer interest-bearing accounts to your clients and to process accrual calculations. In addition to the flexibility and high capacity of Pismo platform processing, this solution offers legal reports.

In this case, work with the Pismo representative to set up interest-bearing accounts.

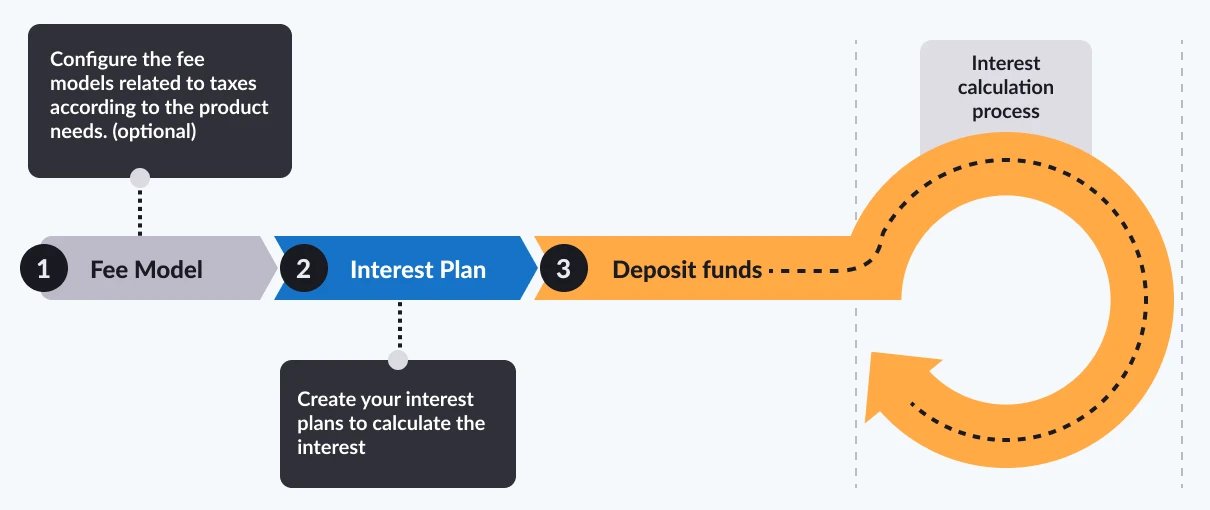

Figure 2: Pismo integration with other banking systems

- If applicable, set up the fee model in the Pismo platform to withhold any taxes or operational fees.

- Configure a flexible plan to accrue interest according to your needs.

- Configure integration with your core banking system.

- Once complete, events are generated to notify you of the interest to be posted. For more information, refer to Output events.

Penalties for deposit products

For penalties associated with deposit products, refer to this table.

| Penalty type | Fee ID | Transaction Flow |

|---|---|---|

| Early withdrawal after opening | earlyWithdrawalAfterOpeningPenaltyID | earlyWithdrawalAfterOpeningPenalty |

| Tiered interest forfeiture | tieredInterestForfeiturePenaltyID | tieredInterestForfeiturePenalty |

| Grace period | gracePeriodPenaltyID | gracePeriodPenalty |

| Withdrawal fee | withdrawalFeePenaltyID | withdrawalFeePenalty |

| Subsequent withdrawal penalty | subsequentWithdrawalPenaltyID | subsequentWithdrawalPenalty |

Refer to Create deposit product for more details.

Output events

The Pismo platform generates events such as Interest accrual succeeded and Interest capitalization succeeded.

Regulatory reports

Contact your Pismo representative for the regulatory reports available in your region.

Examples

Scenario 1

For example, your principal amount is 10,000, the floating interest rate is DI (10.65% for the entire period), the index rate is 103%, the accrual rate is daily, and the payout frequency is daily. The Pismo platform uses your account balance to calculate the daily yield after the cut‑off window and credits the amount to your account on the next business day (D+1), according to your configured settings.

If you make no deposits or withdrawals, your account accrues the following amounts:

• On day 2, the credited amount is 4.13.

• On day 3, the credited amount is 4.13.

• On day 4, the credited amount is 4.14, and so on.

Scenario 2

In this example, your principal amount is 10,000, the fixed interest rate is 6.17%, the accrual rate is monthly, and the payout frequency is monthly. The platform calculates your yield based on your account balance and credits it to your account each month.

If you make no deposits or withdrawals, your account accrues the following amounts:

• For month 2, the credited amount is 50.02.

• For month 3, the credited amount is 50.27.

• For month 4, the credited amount is 50.51, and so on.

Common configuration parameters

The following parameters are common for setting up interest-bearing accounts.

Parameter | Possible values |

|---|---|

|

|

|

|

|

|

|

|

|

|

| You can configure and attach any fee model. For example, you can configure and apply national taxes or custom operational fees. |

Updated about 2 months ago