Full and Zero balance transaction workflows

This guide explains how fund transfers are processed on the Pismo platform through Full balance and Zero balance integration models. These workflows involve three key components: authorization, clearing, and transaction creation.

Authorization (Base I): The initial step where a transaction request is validated and approved by the issuer.

Clearing (Base II): The process of finalizing and posting the transaction after authorization.

Transaction Creation: Recording the transaction details for accounting and reporting purposes.

Throughout this guide, you’ll learn how these steps differ between Full balance and Zero balance integrations, including validation rules, anti-fraud checks, and issuer responsibilities.

Fund transfers into or out of an account generate two types of records:

-

Authorization—A record stating that a given amount was authorized for adding to, or taking from, an account. It contains information about its nature, such as the amount, local currency, date and time, and applicable fees.

In the Pismo authorization workflow:- Authorization/Base I—The initial request to the issuer to approve a transaction process.

- Clearing/Base II—Finalizing and posting the transaction process.

-

Transaction— Belongs to one particular authorization - part of a complete purchase or funds transfer. It can correspond to a purchase installment, a fee amount, a statement payment, or a transfer between accounts, among other things.

Authorization/Base I

The following is the Authorization/Base I workflow for both Full balance and Zero balance integrations.

Note: This guide details the events that Pismo generates during the authorization and clearing process, for more information on these events, refer to Authorization events.

-

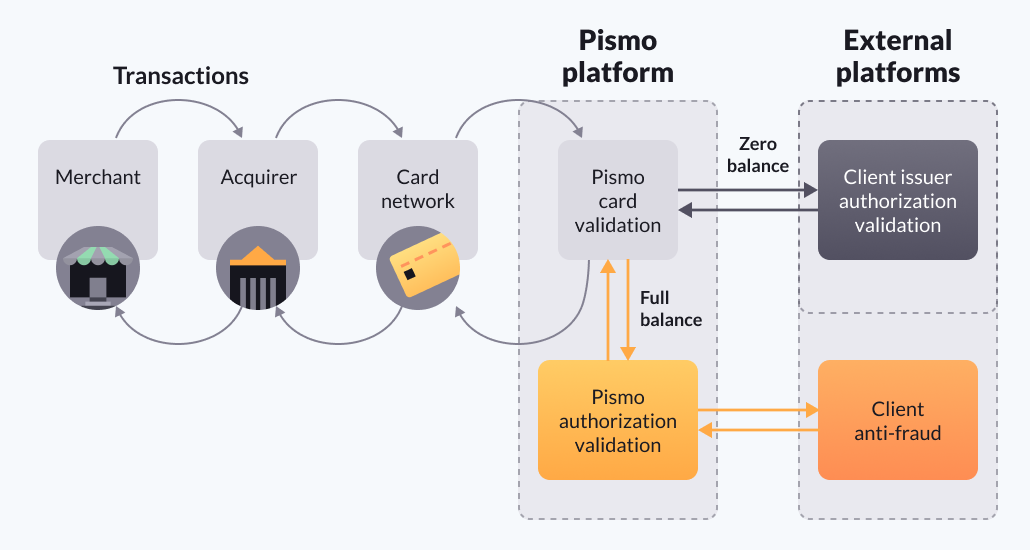

User provides merchant with card information.

-

Merchant's point-of-sale (POS) device or payment gateway formats a message with an authorization request and sends it to the acquirer. Acquirers own most POS devices.

-

Acquirer sends a message to the card network which then sends a message to the processor, the Pismo platform.

-

Pismo removes sensitive data from the message and generates a Network authorization ISO8583 message received event.

Zero balance receives this event and it also receives the raw message when Pismo calls the issuer's webhook in Step 5. Refer to the Zero balance validations request details to review this call's details.

-

Pismo performs validations and, for Full balance, does anti-fraud and account and balance checks.

- Full balance—Card validations (stateful) plus balance and account checks (stateless) and anti-fraud checks. Pismo calls issuer's anti-fraud webhook with its results which the issuer can override. For more information, refer to Anti-fraud integration. Note that this integration is optional. if you do not provide a webhook, Pismo responds to the network with its own results.

- Zero balance—Basic validations - Primary Account Number (PAN), Card Verification Value (CVV), etc. (stateless). If card validation fails, go to step 6, Pismo does not need to call the issuer in this case. Otherwise, Pismo calls the issuer's webhook so they can do their own anti-fraud checks and account and balance checks. Refer to Zero balance anti-fraud and validations integration for more information.

- Response time—For both Full and Zero balance customers, the issuer has 2 seconds to respond to a customer webhook call.

- Validations—For more information on validations, refer to Authorization validation rules.

- Pismo gets response message from issuer (if called) and responds to network. Pismo generates a Network authorization received event and a Card network authorization return sent event.

- The card network sends back the response to the acquirer, who then sends the message to the merchant.

Clearing/Base II

Pismo downloads the Clearing/Base II files and generates a Network authorization clearing message received and additional raw_ messages. Refer to clearing messages for more information.

- For Full balance customers, Pismo does all accounting, ledger, and credit and debit settlement. It also generates a confirmation Network authorization received event.

- Zero balance customers get the clearing events, but have to do their own account and balance settlement.

For more information, refer to Clearing/Base II.

Transaction creation

- Full balance—For an approved authorization, Pismo creates a transaction and generates a create transaction event.

- Zero balance—Issuers need to create the transaction themselves.

Updated about 2 months ago