Loan management overview

After you create a loan booking, the loan becomes active and the borrower starts making payments.

For the end-to-end sequence across product setup, simulation, booking, disbursement, repayment, and settlement, refer to Lending journey in Lending overview.

When you simulate or book a new loan, the Pismo platform generates a repayment schedule based on the configurations of the associated loan product. The repayment schedule is an array containing details about each repayment period, including the amount to be paid, any fees being charged, the due date, and the remaining balance. You can retrieve a repayment schedule by loan ID using the List account loans endpoint.

Loan repayment scenarios

Loan repayment behavior varies depending on the loan product and the repayment schedule generated when the loan was booked. In general, the following configurations impact repayment behavior:

- The loan amount

- The repayment due date

- If repayment is made at the beginning or end of the period

- If loan charges are paid upfront, deducted from the disbursement, or amortized over the life of the loan

- If interest is charged, and how it is repaid over the life of the loan

- If stages are used to change these configurations after a set number of periods

For more information on configuring loans and loan products, refer to Create loan products.

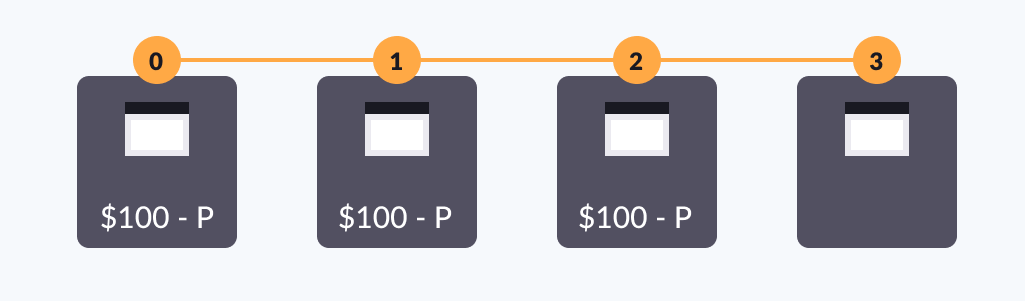

Example 1

The following diagram shows a zero-interest, no-charge loan with repayments at the beginning of each period. For a loan of $300 to be repaid in three months, the borrower pays three flat payments of $100 each. (A payment period could represent a week, a fortnight, a month, or a quarter.)

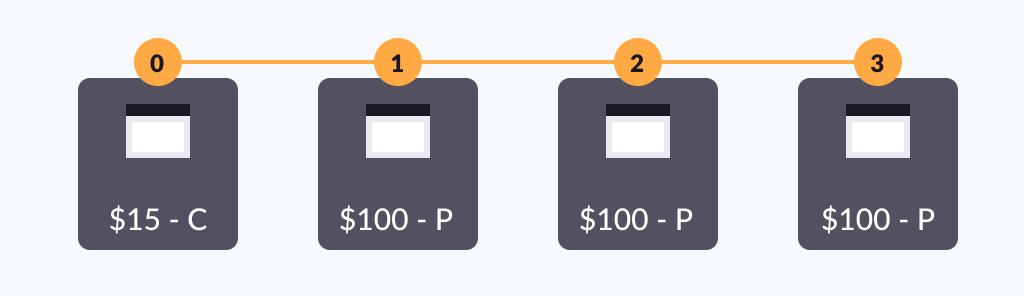

Example 2

The following diagram shows a zero-interest loan with upfront charges and repayments at the end of each period. For a loan of $300 with a 5% charge to be repaid in three months, a $15 fee is charged up front at the time of booking, followed by flat payments at the end of the first three payment periods of $100 each.

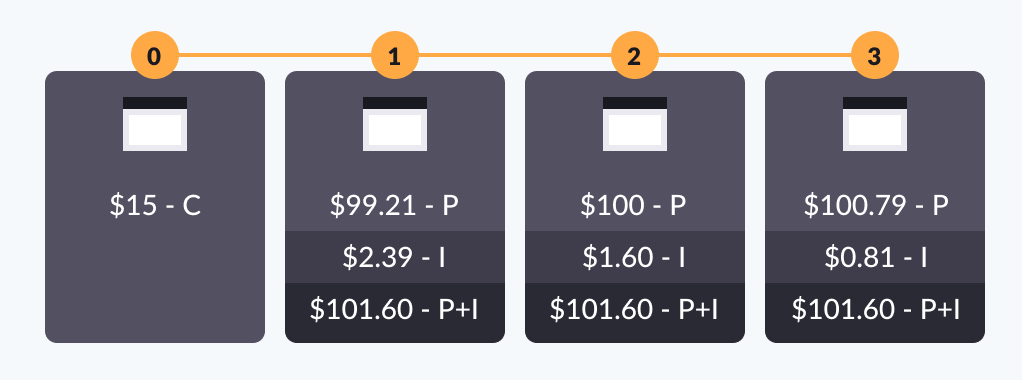

Example 3

The following diagram shows a loan with charges deducted from the disbursement and interest calculated on a reducing balance basis. For a loan of $300 with a 5% charge and 10% interest per year to be repaid in three months, the repayment lifecycle includes:

- A $15 charge deducted from the disbursement

- A flat total repayment amount, where the amount of interest repaid is greatest in the first period and reduces each period after that

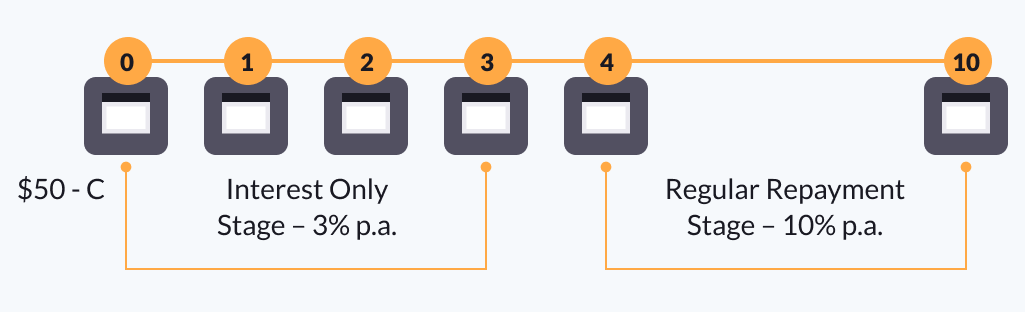

Example 4

The following diagram shows a loan with multiple stages, deducted charges, and interest calculated on a reducing balance basis. The first stage lasts three periods and only charges the borrower for an interest rate of 3% per year (represented with p.a. or per annum in the following diagram). The second stage lasts seven pay periods and charges the principal and interest at a rate of 10% per year. For a loan of $1000 with a 5% charge and 3% interest in the first three periods and 10% interest in the final seven periods, the repayment lifecycle includes:

- A $15 charge deducted from the disbursement

- A flat repayment of the interest only at a rate of 3% for three months

- A flat repayment of the principal and interest at a rate of 10% for seven months, where the amount of interest repaid is greatest in the fourth month (the first period of this stage) and reduces each period after that

Cancellation

A loan cancellation usually occurs when the lender decides the borrower is not qualified or when the borrower decides they do not want the loan.

If a loan is canceled before disbursement, the borrower may not be charged. If a loan is canceled after disbursement, the borrower is responsible for repaying the disbursed amount.

To cancel a loan, use the Cancel loan endpoint and include the ID of the loan as a path parameter. The DELETE command updates the loan’s status to CANCELED; it does not delete the record from the Pismo platform.

Partial repayment

A partial repayment occurs when a borrower does not pay the full amount of the current repayment period. For example, if the borrower owes $300 this month but only pays $200, they have made a partial repayment.

When a borrower makes a partial repayment, the status of the repayment period updates to PARTIALLY_PAID. Before the repayment period’s due date, the borrower can make additional payments until the remaining balance is zero.

If a borrower fails to pay the balance of a repayment period before the due date, the status of the repayment period updates to PAST_DUE. Depending on the loan agreement, a past due repayment may put the loan into default. Borrowers who default on their loan may need to make an arrears payment.

Grace period

A grace period is a number of calendar days after an installment due date during which the Pismo platform does not apply late fees or mark the repayment as delinquent. It is configured on the loan product using the grace_period_days field, which accepts a value between 0 and 365. A value of 0, or omitting the field entirely, means no grace period applies and late fees or delinquency are triggered immediately after the due date. For example, a grace_period_days value of 7 gives the borrower seven additional calendar days to pay before any penalties are applied. If the last day of a grace period lands on a preset holiday, the platform extends the grace period by one day.

Early settlement

Early settlement or early final settlement (EFS), occurs when a borrower repays the full amount of a loan (plus any charges incurred) before the final scheduled payment date.

To initiate an early settlement, you must first simulate the details of the final settlement payment. The simulation calculates any repayment penalties that must be repaid in the final payment. To simulate an early settlement, use the Simulate early final settlement (EFS) endpoint.

After the borrower has reviewed the details of the simulation, you can use the Register early final settlement endpoint to confirm and apply the simulation details to the loan and accept the early settlement payment.

Depending on the loan product, the borrower may not be able to initiate an early settlement for a set period of time, or the borrower may incur a penalty fee when making the final payment. Rules and penalties for early settlement are defined in the loan product.

You can define the following rules for early settlement:

- Penalty rate: A penalty applied as a percentage of the remaining balance.

- Number of periods: The number of payment periods to include when calculating the early settlement penalty. If this is set to zero, the early settlement penalty is calculated using the number of remaining payment periods before the original settlement date.

- Blackout period: The number of payment periods that must be completed before an early settlement can be made.

The Pismo platform calculates the penalty (if any) for early settlement by multiplying the remaining balance of the loan by the penalty rate, then multiplying that by the number of periods defined in the loan product (or the number of periods remaining for the loan). For example, a $200 loan with a $100 balance, 10% penalty rate, and 3 remaining payment periods would incur a penalty of $30 (100 x .1 x 3 = 30). The final settlement balance would be $130.

You also have an option to waive penalty for early settlement.

Updated 3 days ago